Pakistan’s E-Commerce Market Size Exceeded $600 Million in 2017

The State Bank of Pakistan has released their official numbers showing the actual size of the e-commerce market. Before delving into its analysis, let us first take a look at the numbers in full.

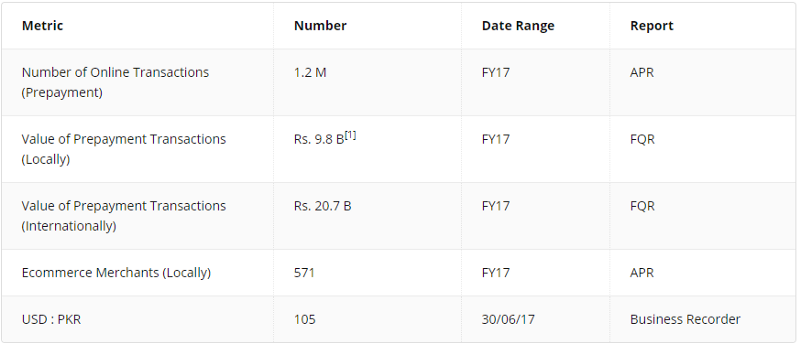

Data Sources

The two primary sources of the data are:

Annual Performance Review (APR) 2016–2017 — Payment Systems — link

First Quarterly Report (FQR) 2017–2018, Special Section 2 — Online Payments Platform — link

Quick Analysis

Based on the report, we can deduce that, on average, every prepayment order in Pakistan had a basket size greater than Rs. 8,000 and each of the 571 merchants processed about Rs. 17M in prepayment orders on average.

Judging the “Cash on Delivery” Market Size

Not all e-commerce transactions are done through pre-payment. For instance, in the large marketplaces and brand stores, most of the payments are made via cash on delivery terms. To accurately gauge the e-commerce market size, we have to make an assumption on the volume of transactions processed via Cash on Delivery (COD).

Most of the other industry professionals claim that payments made through Cash on Delivery account for about 90% of all e-commerce transactions. However, that figure represents the number of transactions rather than the volume of transactions.

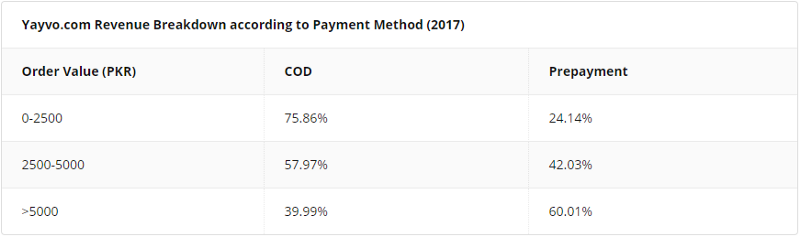

In my analysis, I have found that customers are more likely to pay for higher value orders via prepayment rather than COD. Yayvo, for example, had 76% of its orders below Rs. 1500 paid via COD, while 60% of its orders above Rs. 5000 were paid via prepayment.

I still believe that during the Fiscal Year 2017, the market was still very nascent to the idea of prepayment. I would estimate that COD was at minimum 85% of the total market for payments. This means that the e-commerce market size in Pakistan is ~Rs. 65 Billion or ~$620 Million.

Other Assumptions

Not all e-commerce sites process their online payments in Pakistan. Within the fiscal year ending in 2017 (July 2016 — June 2017), large e-commerce players such as Careem, Uber, and FoodPanda processed their payments via international gateways. Their prepayment revenue is unlikely to be counted within the local e-commerce market size but is counted in the international volume of transactions instead.

I am assuming that there was no duplication of the online acquirers when the State Bank was collecting this data. For example, JazzCash and EasyPay both used the MCB e-Gateway to power their platforms during this period. I am assuming that the State Bank did not count these numbers twice when collecting the figures submitted by EasyPay/JazzCash and MCB respectively. This is especially important given that EasyPay had over 350 merchants and JazzCash over 150 merchants by June 2017, which possibly makes them the largest online acquirer’s in Pakistan.

E-commerce Merchants

According to the State Bank, there are 571 e-commerce merchants in Pakistan. Typically, the e-commerce merchants that come to mind are players such as Daraz.pk and Yayvo.com. We have to dismiss players like FoodPanda, Careem, and Uber because their payments are not processed in Pakistan.

Other large merchants include ticketing platforms such as Pakistan Railway and PIA, amongst others. Pakistan Railway, in its first two months, reported a revenue of Rs. 100M from online sales. In addition, an article in November 2017 stated that UBL had made more than Rs. 1 Billion from online sales through Pakistan railway alone.

Conclusion

The overall e-commerce market size is much bigger than what many industry insiders estimate. After reviewing and examining the numbers, my conclusion is that the e-commerce market size transcended $600M in the 12-months period between July 2016 and June 2017.

I believe the number will be much higher in the current financial year (June 2017 to July 2018). A case in point is Yayvo, which is on course to grow their revenue by at least 3x this year. Therefore, the overall market, even with 2x growth, would rise to approximately $1.2 Billion. This means we will be crossing the $ 1 Billion e-commerce revenue mark two years before the 2020 deadline we had set.

[1] There is a difference in the volume of transactions indicated in the two reports. I will be taking into account the numbers given in the FQR because those stated in the APR are provisional. However, the FQR does not show the number of transactions (my assumption is that they would have risen). Therefore, since the FQR does not give full information, I will use the APR numbers.